A lot of people assume foreclosure ends the moment the home is “sold.” In Illinois, that’s usually not true. There are steps after the sale that matter—especially the order confirming the sale, the possession timeline, and whether the lender is seeking a deficiency judgment.

If you’re still in the home (or you have tenants), the biggest risk is acting on bad assumptions. The safest move is to understand the sequence so you can plan housing, protect your rights, and avoid costly mistakes.

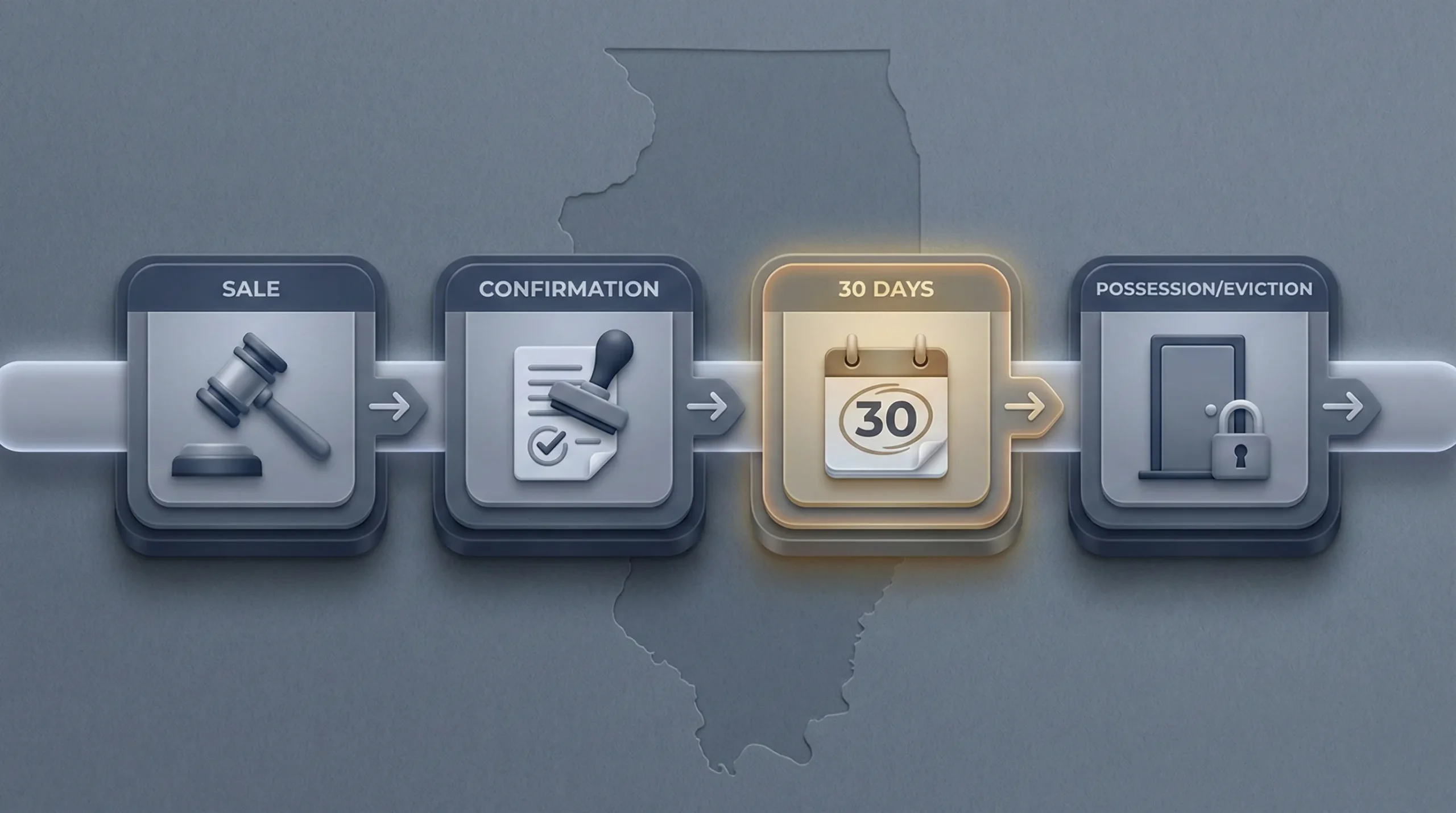

Important timing concept:

In Illinois, the purchaser is generally entitled to possession 30 days after the court enters the order confirming the sale (unless the purchaser consents otherwise). That date often becomes the real “move-out” pressure point—not the auction date itself.

Below is a practical roadmap you can use like a checklist. If you need help reading your specific order, docket, or sale paperwork, a case-specific consult is the fastest way to reduce uncertainty.

Need a Next-Step Plan?

Send your most recent order or notice. We’ll help you understand what happens next and what deadlines matter most.

Step 1: Separate “Judgment,” “Sale,” and “Confirmation”

Homeowners often hear three milestones as if they’re the same thing. They’re not.

- Judgment of foreclosure: the case is moving toward a sale track if it isn’t resolved.

- Sheriff’s sale (auction): the property is bid on, but court approval still matters.

- Order confirming sale: the court approves the sale results and enters key post-sale terms.

In plain English: the auction is a major event, but the

confirmation order is often where the post-foreclosure consequences become real—possession timing, deficiency language, and next procedural steps.

Why Confirmation Is the “Pivot Point”

In many Illinois cases, the confirmation stage is where you learn:

- Whether the court confirmed the sale as conducted

- Whether a deficiency judgment is being entered (if sought and proven)

- When the purchaser is entitled to possession

If you’re unsure what your confirmation order says, don’t guess. The specific language and dates can change how much time you truly have.

Practical tip:

Save a PDF of your Order Confirming Sale and highlight two things: (1) the entry date, and (2) any paragraph about possession or deficiency. Those lines often answer 80% of your urgent questions.

If you want context on the earlier parts of the process, see our related guides:

- What Is Mortgage Foreclosure?

- The Foreclosure Timeline in Illinois

- What Are My Foreclosure Options?

Step 2: What Happens Right After the Sheriff’s Sale

After the auction, the sale is typically reported back to the court. Then a party moves for confirmation. This is where the case shifts from “foreclosure in progress” to “post-sale consequences.”

Depending on the file, you may see additional paperwork about the deed/certificate, fees/costs, and scheduling for the confirmation hearing.

Plain-English translation:

The sale is the bid. Confirmation is the court’s “yes.” Many deadlines and rights become clearer once the court enters the confirmation order.

If you believe something went wrong at sale or confirmation, timing matters. Post-sale challenges are not something to delay—because once possession timing starts running, the practical reality changes quickly.

Sale Already Happened?

Post-sale strategy still matters. A quick file review can clarify possession timing, deficiency risk, and your cleanest exit options.

Step 3: Possession and Eviction Timing in Illinois

In Illinois, the purchaser’s right to possession is governed by the Illinois Mortgage Foreclosure Law. In many cases, the purchaser becomes entitled to possession 30 days after entry of the order confirming sale (unless the purchaser consents otherwise).

That doesn’t always mean the sheriff arrives on day 31—but it often means the purchaser can start the steps needed to remove occupants who remain in the property.

What “possession” can look like in practice:- Written communications from the purchaser or its attorney

- Requests for access, inspections, or repairs

- Eviction filings (especially if occupants were not named parties)

- Sheriff enforcement later if an eviction order is entered

Tenants and Occupants: The Rules Change (Especially in Chicago)

If the property is occupied, the post-foreclosure phase can create confusion. Two big buckets matter:

- Tenants: people renting under a bona fide lease

- Occupants: people in the property who may not be tenants or may not be named in the foreclosure case

Tenants often have protections that survive the sale, including federal protections under the

Protecting Tenants at Foreclosure Act (PTFA) and local protections in Chicago.

In Chicago, the Keep Chicago Renting Ordinance (KCRO) can require the new owner of a foreclosed rental property to either offer a lease through good-faith negotiation or pay relocation assistance to qualified tenants (commonly referenced as $10,600 per qualified tenant household).

If you’re the former owner and your building has tenants, it’s smart to communicate calmly, avoid threats, and avoid “self-help” behavior. The way occupancy is handled can create side disputes that make everything worse.

Money After Foreclosure: Deficiency, Liens, and Credit

For many homeowners, the second shock is financial: “Do I still owe anything after I lose the home?” Sometimes, yes.

In Illinois, the confirmation order can also include a personal deficiency judgment if requested in the complaint and properly proven—meaning the lender seeks the difference between what’s owed and what the property sold for (subject to the case specifics).

Three things to check immediately:- Deficiency language: does the confirmation order include a personal money judgment?

- Second liens: were HELOCs/seconds addressed or do they remain as separate issues?

- Credit reporting: what was reported, and is there a negotiated path to cleanup in your resolution?

If you’re planning your “after” strategy, you may also want to read:

- Restoring Your Credit After Foreclosure

- Pre-Foreclosure Sales

Your Practical Post-Foreclosure Checklist

Whether you’re the homeowner or a landlord dealing with occupancy, the post-foreclosure period is mostly about reducing risk and regaining control. The best next steps are usually simple and document-driven.

Checklist you can start today:- Get the confirmation order: save it, print it, highlight entry date.

- Calculate the 30-day mark: that’s often the possession pressure point.

- Document occupancy: who is living there, tenant vs. occupant, what leases exist.

- Secure your records: photos, communications, payment history, modification/submission proof.

- Plan housing: don’t wait for a crisis week—start mapping options now.

- Confirm deficiency risk: read the order for personal judgment language.

What not to do:- Don’t rely on verbal promises like “nothing will happen while we review your file.”

- Don’t ignore notices from the purchaser or its attorney.

- Don’t attempt “self-help” lockouts or utility shutoffs if tenants are involved.

If you’re trying to keep the home, post-sale options can be limited and time-sensitive—so you want guidance quickly. If you’re exiting, your goal is a controlled landing: fewer surprises, fewer loose ends, and a plan for what happens next.

When EV Häs Can Help After Foreclosure

Even after sale, legal strategy can still matter. Depending on your facts, counsel may be able to help you understand the file, respond correctly to post-sale steps, reduce the chance of avoidable judgments, and plan a safer exit timeline.

If you’re feeling stuck, start here:

Bring your case number, your confirmation order (if entered), and any notices you’ve received from the purchaser or servicer.

If tenants are involved, we can help you understand what the new owner may be required to do and what you should avoid doing so you don’t create side litigation on top of an already stressful situation.

Reminder: This page is educational only and not legal advice. Your next step should be based on your specific court file, timeline, and goals.

Tenants in the Property?

If your building is occupied, you need to handle notices and transitions carefully—especially in Chicago. We can help you avoid preventable mistakes.

Frequently Asked Questions

Quick answers for homeowners and landlords navigating the post-foreclosure phase in Illinois.

Written By: